Table of contents

Click the links below to jump to different sections of the newsletter. To view a PDF version of the shorter print edition of the newsletter, click HERE.

If you wish to support PNHP’s outreach and education efforts with a financial contribution, click HERE.

If you have feedback about the newsletter, email info@pnhp.org.

PNHP News and Tools for Advocates

- SNaHP students pass neutralization resolution at the AMA-MSS

- PNHP members host 35th anniversary house parties

- House party attendance and donations … make it fun!

- Medicare for All bills introduced in Congress

- PNHP wins crucial victory against ACO REACH

Save the Date: Nov. 10-12 in Atlanta

Research Roundup

- Data Update: Health care crisis by the numbers

- Studies and analysis of interest to single-payer advocates

PNHP Chapter Reports

SNaHP Chapter Reports

How You Can Support the Medicare for All Act

PNHP in the News

PNHP News and Tools for Advocates

SNaHP Students Pass Single-Payer Neutralization Resolution at AMA Medical Student Section

Four years ago, SNaHP students and community allies led an action at the annual meeting of the American Medical Association (AMA). The aim was to expose the AMA’s involvement in the Partnership for America’s Health Care Future, a dark money lobbying group that pulled together some of health care’s biggest profiteers to spread misinformation about Medicare for All.

Activists rallied outside the AMA meeting and organized a die-in during the opening ceremonies, garnering significant attention from media, political figures, and physicians as to the AMA’s inclusion in the insidious collective. Shortly after, the AMA was forced to withdraw from the partnership.

While getting the AMA out of the group was a huge victory, it remains a stubborn obstacle to the advancement of the single-payer movement and does not represent the true views of the majority of doctors across the country. That is why four years after their initial action, a group of SNaHP students have successfully passed a resolution at the AMA Medical Student Section calling on the AMA to remove all anti-single payer language from its stances and drop its decades-long opposition to Medicare for All.

SNaHP students worked on this effort for months, researching the resolution process, planning out their testimony, and establishing plans for every potential scenario at the meeting. Their work paid off, and the resolution passed unanimously.

“Surveys show that more and more physicians are open to the idea of a single-payer system,” said Donald Bourne, an M.D./Ph.D. student at the University of Pittsburgh and a member of the resolution group. “It’s time our AMA updates its policies in accordance with the viewpoints of its membership.”

Now that the resolution has passed, the next goal is to get it through the AMA House of Delegates and ensure that the AMA entirely retracts its opposition to single payer. This will lay the foundation for a campaign to have them fully and openly endorse improved Medicare for All, and finally become a true representative for our physicians.

If you are interested in helping lead an effort to get a single-payer resolution passed in any medical society you are a member of, fill out our campaign interest form HERE. Questions? Email lori@pnhp.org for more information!

Members Host House Parties for PNHP’s 35th Anniversary

As part of our 35th anniversary campaign, PNHP is raising funds for a variety of important goals. During our first phase, we sought to build support for our SNaHP student activists, and in the second, we are digging deep on efforts to protect Medicare from privatization. Several PNHP members have hosted house parties with like-minded colleagues, family, and friends to raise money for our initiatives and introduce more people to PNHP and the Medicare for All movement.

We interviewed members to learn more about their experience hosting a party for PNHP. If you are interested in hosting but unsure how to get started, check out these tips!

If you have additional questions, please contact lori@pnhp.org for more information on how to get started.

Getting House Party Attendance and Donations … Make it Fun!

“We featured food from countries with universal health care! Poutine (Canada), sushi (Japan), Chinese (Taiwan), pasta (Italian), and pretzels/pretzel dough balls (Germany), with wine/beer only from such countries. We let people arrive and mingle, and then around 6, we gathered for a short presentation and then a stimulating discussion about single payer and issues at both the local and national level. Have fun with it, don’t stress, and be flexible!” – Dr. Philip Verhoef, HI

“It was great to have a co-host to help with invites (together we invited over 150 people) and coordinating food. We asked people who we know are interested in the issue, although not necessarily health professionals, and invited many people we know through our connections with the local Democratic party. Having margaritas to drink helped also!” – Dr. Eve Shapiro, AZ

“We did a phone banking session to reach out to members, and also sent out digital invites. We additionally created a 4-person Host Committee that was responsible for sending a separate invitation to 10-15 potential donors. We held the event at a local tavern and had some appetizer platters and custom PNHP 35th Anniversary cake and cookies. We had a book display and several activities that served as conversation starters: a single payer board where attendees could vote on the strongest argument for single-payer healthcare, a wheel to spin for PNHP merch and free drinks, and other games. I would encourage people to team up with a co-host or two as that can really increase the odds of having more people attend and donate.” – Dr. Belinda McIntosh and PNHP Georgia

Medicare for All Bills Introduced in Congress

In May, Sen. Bernie Sanders and Reps. Pramila Jayapal and Debbie Dingell introduced in both houses of Congress the Medicare for All Act of 2023. Senator Sanders and Representative Japayal held a town hall meeting before the bill was introduced, where PNHP leaders Dr. Adam Gaffney and Dr. Sanjeev Sriram spoke on the need for this crucial legislation.

“As a critical care physician, I have seen patients with life-threatening illnesses from chronic conditions that were not treated because they could not afford the care,” said Dr. Gaffney. “Medicare for All will solve that.”

Dr. Sriram remarked on the latest crisis in American health care, as the Medicaid unwinding process threatens to remove insurance coverage for millions of vulnerable families and children. “If you don’t pick up the phone at the right time, or if you don’t fill out a form correctly,” he said, “your family and your kids could lose your Medicaid. We need a better system.”

The Medicare for All Act of 2023 includes a number of improvements and changes to the previous version of the bill in the areas of women’s and LGBTQ+ health, which have both been under attack across the country. All reproductive health care, including abortion care and contraception, are now explicitly covered under this legislation, and the same is true of all gender affirming care.

“These additions are extremely important to me as a physician, an activist, and an advocate for women’s health,” said PNHP Vice President Dr. Diljeet Singh. “Given the current campaign against women and the LGBTQ+ community in the U.S., it is crucial that we stand up for their right to access these necessary and often lifesaving treatments.”

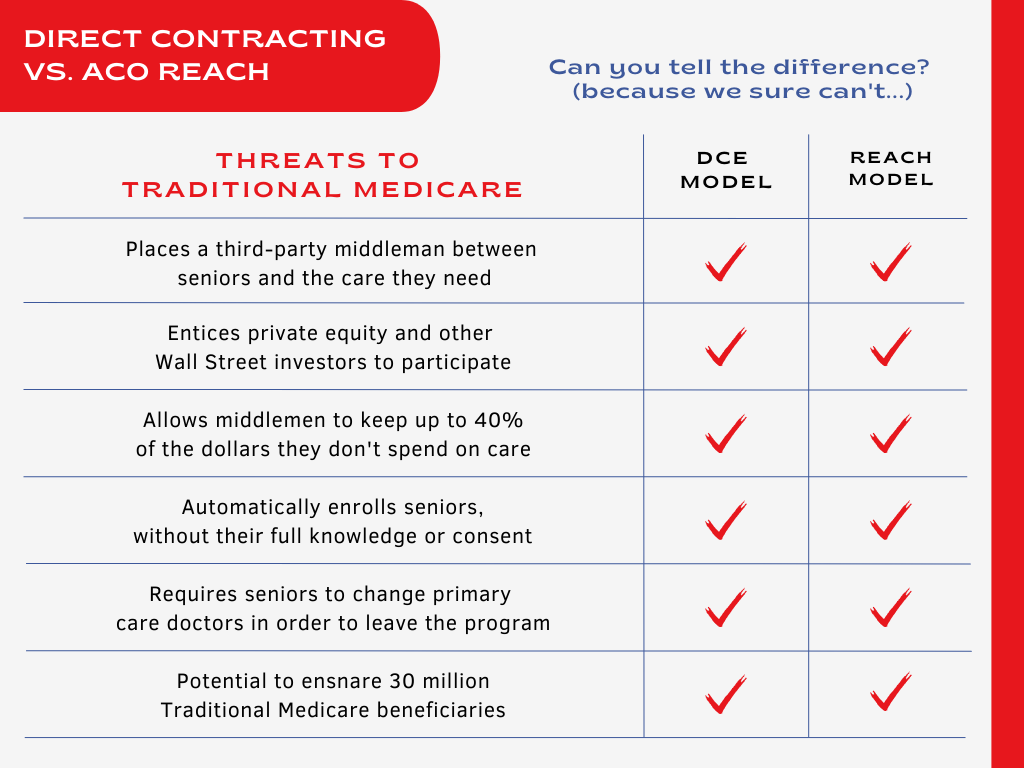

PNHP Wins Crucial Victory Against ACO REACH

Since the inception of Direct Contracting in the final days of the Trump administration, and its rebranding as the REACH program by the Biden administration in early 2022, PNHP has led the charge against this dangerous attempt to privatize Traditional Medicare. REACH allows third-party entities (often private insurers) to administer Traditional Medicare benefits. Under this program, seniors and people with disabilities who specifically choose a government-run plan are instead pushed into private management, often without their knowledge or consent.

PNHP was quick to recognize the dangers of REACH, and put together a coalition of over 300 grassroots organizations from across the country to demand an end to the program. We were joined in our efforts by members of Congress like Rep. Pramila Jayapal, as well as thousands of individual activists. Together, we applied consistent pressure on the Biden administration to end REACH and save Medicare from further corporate encroachment.

After months of campaigning, our work paid off. In a speech given to the California Public Employees’ Retirement System (CalPERS) on January 17, Center for Medicare and Medicaid Innovation (CMMI) Director Liz Fowler revealed that there are no plans to further expand the number of organizations or beneficiaries in the controversial model.

While the fight to end the program immediately and permanently is not over, PNHP’s victory on REACH demonstrates the power of our activism and the importance of fighting to protect Medicare as the necessary foundation for a true single-payer health care system. We will continue these efforts as we mount a campaign against rampant profiteering in the Medicare Advantage program.

Save the Date: Nov. 10-12 in Atlanta

Join us for PNHP’s in-person Annual Meeting, Leadership Training, and SNaHP Summit—scheduled for Nov. 10-12 in Atlanta.

Celebrate 35 years of single-payer advocacy with a weekend of learning, strategizing, and organizing … as well as our special 35th anniversary dinner on Sat., Nov. 11.

Research Roundup

Data Update: Health Care Crisis by the Numbers

Barriers to Care

Family caregivers report worse experiences with for-profit hospice care: A survey of over 600,000 respondents across 3107 hospices found that caregivers reported worse experiences on all measures at for-profit hospices compared to non-profit hospices. Overall, 31.1% of for-profit hospices rated 3 or more points below the national average rating, compared to just 12.5% of non-profit hospices. Additionally, more non-profit hospices were highly rated, with 33.7% of non-profit hospices scoring 3 or more points above the national average and only 21.9% of for-profit hospices doing the same. Price et al., “Association of Hospice Profit Status With Family Caregivers’ Reported Care Experiences,” JAMA Internal Medicine, 2/27/2023.

More paid sick leave leads to more cancer screenings: In areas with policy-driven paid sick leave mandates, breast cancer screenings increased up to 4% and colorectal cancer screenings increased between 6-8%. Looking solely at workers who were gaining sick leave for the first time under new mandates, breast cancer screenings went up 9-12% and colorectal cancer screenings went up 21-29%. Callison et al., “Cancer Screening after the Adoption of Paid-Sick-Leave Mandates,” New England Journal of Medicine, 3/2/23.

Long COVID patients more likely to struggle with care access: Adults with post-COVID-19 condition (PCC, or long COVID) were more likely to report challenges meeting health care needs when compared with adults never diagnosed with COVID, or who had COVID but recovered. Adults with long COVID were more likely to report issues with cost (27% vs 18.3% and 17.5%), finding clinicians accepting new patients (16.4% vs 10.1% and 10.7%), getting a timely appointment (22% vs 14.4% and 13.9%), and getting health care authorization (16.6% vs 10.8% and 10.3%). Karpman et al., “Health Care Access and Affordability Among US Adults Aged 18 to 64 Years With Self-reported Post–COVID-19 Condition,” JAMA Network Open, 4/10/23.

Access to gender-affirming care is in increasing danger: 19% of transgender youth live in states where gender-affirming care for children is banned. At least 11 states exclude coverage of gender-affirming care in state Medicaid programs, while 15 states ban care for transgender youth entirely. In the first three months of 2023, more bills have been introduced attacking transgender health care than in the last 6 years combined. In April of 2023, Missouri became the first state to effectively ban care for all transgender people, regardless of age. Movement Advancement Project, “LGBT Policy Spotlight: Bans on Medical Care for Transgender People,” April 2023.

After Roe, Americans report abortions as harder to get: 54% of Americans say it would be very easy or somewhat easy to get an abortion where they live, down from 65% in 2019. 42% say it would be very difficult or somewhat difficult, up 10% from 2019. 34% of adults say that abortions should be easier to access in the area where they live, an increase of 8% from 2019. 62% of Americans say that abortion should in general be legal in all or most cases, largely unchanged from four years ago. Pew Research Center, “Nearly a Year After Roe’s Demise, Americans’ Views of Abortion Access Increasingly Vary by Where They Live,” 4/26/23.

Medical debt associated with significantly higher cancer mortality: For every one percent increase in the population with medical debt, there was a 1.12 increase in death rates (per 100,000 person-years) from cancer. The highest increases associated with medical debt were seen in lung cancer, colorectal cancer, and female breast cancer. In counties where the exact amount of medical debt was known, for every $100 increase in the median debt carried by the population, there was a statistically significant increase of 0.86 per 100,000 person-years in age-adjusted mortality rates for all malignant cancers. Hu et al., “Association of medical debt and cancer mortality in the US,” Journal of Clinical Oncology, 5/31/23.

Higher co-pays for heart failure and diabetes medications lead to nonadherence: Insured patients with heart failure and diabetes who had high or medium co-pays for their medications (defined as greater than $50 or between $10 and $50) were less likely to have an adequate level of medication adherence than those with low co-pays (defined as less than $10). For GLP1-RA therapies like Trulicity, adherence was achieved for 71.9% with a low co-pay, 65.7% for a medium co-pay, and 59.9% with a high co-pay. For SGLT2i therapies like Farxiga, adherence was achieved for 77.1% with a low co-pay, 71.5% with a medium co-pay, and 72.1% with a high co-pay. Essien et al., “Association of Prescription Co-payment With Adherence to Glucagon-Like Peptide-1 Receptor Agonist and Sodium-Glucose Cotransporter-2 Inhibitor Therapies in Patients With Heart Failure and Diabetes,” JAMA Network Open, 6/1/23.

Medical debt burdens 1 in 10 adults in Los Angeles county: 810,000 residents of the county owe a total of more than $2.6 billion as of 2021. Medical debt in the county disproportionately affects the uninsured and underinsured, low-income residents, and Black and Latino populations, and negatively impacts factors such as housing, employment, food security, and access to prescriptions and health care. Roughly 30% of adults with trouble paying medical debt owe less than $1,000. About half of those who took on credit card debt to pay off the bills or were unable to pay for necessities owe less than $2,000. Work, “Personal Medical Debt in Los Angeles County Tops $2.6 Billion, Report Finds,” KFF Health News, 6/7/23.

Medicare & Medicaid Issues

Arkansas plans shortest Medicaid redetermination timeline: Although more than one-third of Arkansas’ three million residents depend on Medicaid, state officials announced plans to complete the redetermination process in just half a year, raising fears that many in the state will be kicked off the rolls despite still being eligible. In 2018, new Medicaid work requirements in Arkansas led to an estimated 140,000 people losing coverage, despite 95% of those affected still being eligible. Over 420,000 people have been identified by the state as appearing to be ineligible and needing to go through redetermination, with an additional 240,000 going through the regular renewal process over the year. Messerly, “Why one state’s plan to unwind a Covid-era Medicaid rule is raising red flags,” Politico, 2/27/2023.

Medicare Advantage now covers half of all eligible beneficiaries: Of the 59.8 million people in Medicare Part A and B, 30.2 million are on a private plan. In 2007, just 19% of the eligible population was in the program, but that figure has grown steadily each year. In 2021, MA enrollees submitted a total of 35 million prior authorization requests. Biniek et al., “Half of All Eligible Medicare Beneficiaries Are Now Enrolled in Private Medicare Advantage Plans,” KFF, 5/1/23.

Early Medicaid unwinding data shows disenrollment is largely procedural: Of those evaluated, the disenrollment rate ranges from 10% in Virginia to 54% in Florida. In Indiana, West Virginia, Arkansas, and Florida, more than 80% of those taken off the rolls lost coverage due to procedural reasons rather than changing eligibility. In Florida alone, nearly 250,000 people have lost their Medicaid coverage. Tolbert et al., “What Do the Early Medicaid Unwinding Data Tell Us?” KFF, 5/31/23.

Medicare Advantage overpayments lead to huge insurer profits: A significant portion of the $2.8 billion insurer Humana made in profit in 2022 was due to Medicare Advantage overpayments, and without those payments, it could have suffered a loss of as much as $900 million. In total, the federal government overpaid an estimated $20.5 billion to private insurers running Medicare Advantage plans. Because of these overpayments, Medicare costs from 2023 to 2031 will be $600 billion higher than if Medicare Advantage beneficiaries were instead enrolled in traditional Medicare. Cunningham-Cook and Perez, “The $20 Billion Scam At The Heart Of Medicare Advantage,” The Lever, 5/26/23.

Medicaid is crucial for improving health equity: Large proportions of groups of color depend on Medicaid for insurance coverage. Among adults below 65, 29% of Black people, 22% of Hispanic people, 33% of American Indian or Alaska Native people, and 38% of Native Hawaiian or Other Pacific Islander people are on Medicaid. The numbers are even higher for minors, with 60% of Black children, 55% of Hispanic children, 59% of American Indian or Alaska Native children, and 52% of Native Hawaiian or Other Pacific Islander children on Medicaid. Hispanic and Black people are predicted to be disproportionately affected by the disenrollment process, and face greater rates of churn in renewing coverage. Medicaid expansion has helped reduce racial and ethnic disparities in coverage, and of the 1.9 million people in a coverage gap in non-expanding states, 32% are Black and 24% are Hispanic. In general, nearly two-thirds of the 7.4 million people eligible for Medicaid but not enrolled are people of color. Guth et al., “Medicaid and Racial Health Equity,” KFF, 6/2/23.

Pharma

Eli Lilly avoids Medicaid rebates by cutting insulin prices: A provision in the Inflation Reduction Act forces drug producers to pay Medicaid rebates when they increase the price of drugs faster than the rate of inflation. An additional provision in the American Rescue Plan removes a cap on the price of these rebates, which currently are restricted to the drug’s list price, in 2024. To avoid having to pay Medicaid $150 per vial of Humalog, Eli Lilly lowered the price of the drug by 70%, and additionally lowered the price of its biosimilar drug Lispro to $25 a vial, after years of dramatically raising prices for both medications. Wilkerson, “By cutting insulin prices, Eli Lilly avoids paying big Medicaid rebates,” STAT News, 3/6/23.

Foundation charges $83,000 for unproven cancer drug: The medication, a customized five-month series of vaccine shots, costs $83,000 out of pocket and is being sold under an FDA policy that allows drugmakers to charge patients for unproven medicines under compassionate use (although actually charging patients in such cases is rare). So far, 26 patients have ordered the drug. The drug is reported to be promising by scientists but has no guarantee of success. Saltzman, “Foundation stirs controversy by charging cancer patients $83,000 for unproven but promising experimental drug,” Boston Globe, 3/4/23.

Biden administration fines 27 drugmakers for price increases: For raising the prices of medication faster than the rate of inflation, the administration will fine drugmakers Pfizer, AbbVie, Gilead, Endo, Leadiant Biosciences, and Kamada. Pfizer had the highest number of medications on the list, with five drugs named (and one more made by a company Pfizer recently acquired for $43 billion). The drugmakers will have to pay Medicare back by the amount the price hike exceeded inflation, though the actual payments will not be due until 2025. Cohrs, “Biden administration to fine manufacturers of 27 medicines for price hikes,” STAT News, 3/15/23.

Moderna plans to increase price of vaccines: Following the end of COVID-19 emergency provisions, Moderna and Pfizer both plan to increase the price of their vaccines, with Moderna charging $130 a shot up from the $25-30 charged during the pandemic. The U.S. government contributed $1.7 billion toward research and development leading to the company’s vaccine. Moderna CEO Stéphane Bancel reportedly made $398 million last year from a combination of salary, bonuses, and realized gains of stock. The company also repurchased $3.3 billion in shares in 2022. Newman, “Moderna CEO defends price of COVID shot at Senate hearing,” Healthcare Dive, 3/22/23.

Johnson & Johnson proposes settlement for cancer-causing talc powder: The company agreed to pay $8.9 billion to roughly 70,000 plaintiffs to settle claims that its talc powder caused ovarian cancer and mesothelioma. Under this plan, each plaintiff would receive roughly $120,000, while the average medical costs for an ovarian cancer patient are around $225,000. If the presiding judge accepts the deal, 75% of plaintiffs would need to sign off on the offer for it to take effect. In previous litigation regarding the talc powder, Johnson & Johnson faced a verdict of $4.7 billion, later reduced to $2.1 billion after appeals. In 2020, the company settled 1,000 cases for $100 million. Dunleavy, “Johnson & Johnson’s $8.9B bankruptcy settlement is ‘unworkable,’ talc plaintiff lawyer says,” Fierce Pharma, 4/10/23.

Teva to pay $193 million to Nevada in opioid settlement: The settlement concerns Teva’s use of marketing practices that fueled opioid addiction, and follows a nationwide settlement of $4.3 billion with the company last year. Teva’s settlement with Nevada will be paid in installments from 2024 to 2043. From 1999 to 2020, over half a million people in the U.S. have died of drug overdose, with opioids being involved in a significant portion of those overdoses. Pierson, “Teva to pay Nevada $193 million over role in opioid epidemic,” Reuters, 6/7/23.

Health Inequities

Racial disparities in child gun injuries and deaths widened during pandemic: The lowest rate of child shootings was found in non-Hispanic White children, at 0.54 per 100,000 person-years, and the highest rate was found in non-Hispanic Black children, at 21.04 per 100,000 person-years. The Black-White disparity in relative risk grew from 27.45 to 100.66 during the pandemic. The Hispanic-White disparity tripled, and the Asian-White disparity nearly tripled. Overall, there was nearly a 2-fold increase in child firearm assault rates. Jay et al., “Analyzing Child Firearm Assault Injuries by Race and Ethnicity During the COVID-19 Pandemic in 4 Major US Cities,” JAMA Network Open, 3/8/23.

Sudden unexpected infant deaths rise significantly among Black children: Although general infant mortality reached a record low in 2020, sudden unexpected infant deaths (SUID), which include SIDS as well as accidental suffocation or strangulation, did not. The SUID rate for non-Hispanic Black children saw by far the most significant rise, going from 192.1 deaths per 100,00 live births in 2017 to 214 deaths per 100,000 live births in 2020. The ratio of SUID in non-Hispanic Black infants compared to non-Hispanic White infants went from 2.2 in 2017 to 2.8 in 2020. Shapiro-Mendoza et al., “Sudden Unexpected Infant Deaths: 2015–2020,” Pediatrics, 3/13/23.

Maternal mortality in the U.S. continues to increase: Deaths due to pregnancy and childbirth continued to rise significantly in 2021. 1205 women died of maternal causes in 2021, compared with 861 in 2020 and 754 in 2019. The overall maternal mortality rate for 2021 was 32.9 deaths per 100,000 live births, compared with 23.8 in 2020 and 20.1 in 2019. Mortality rates increased across all racial and ethnic groups studied; the rate for non-Hispanic Black women was 69.9, 2.6 times the rate for non-Hispanic White women of 26.6. Hoyert, “Maternal Mortality Rates in the United States, 2021,” National Center for Health Statistics, March 2023.

Poverty is the fourth-leading cause of death in the U.S.: In 2019 alone, 183,000 deaths among people aged 15 years or older were associated with poverty. Poverty caused 10 times as many deaths as homicide. Only heart disease, cancer, and smoking are responsible for more deaths. People living with incomes less than 50% of the U.S. median have roughly the same survival rates as those with greater incomes until their 40s, at which point the two groups diverge and those in poverty die at significantly higher rates. Brady et al., “Novel Estimates of Mortality Associated With Poverty in the US,” JAMA Internal Medicine, 4/17/23.

Racial disparities in premature pandemic deaths: For all groups of color, premature death rates (defined as death before age 75) saw a steeper increase than in White people. From 2019 to 2022, the increase in the Hispanic premature death rate was 33%, compared with 14% for White people. Premature deaths among White people resulted in an average of 12.5 years of life lost, compared to 19.9 years of life for Hispanic people and 22 years of life for American Indian and Alaska Native people. Communities of color make up 40% of the total U.S. population, but saw 59% of the country’s premature pandemic deaths. McGough et al., “Racial disparities in premature deaths during the COVID-19 pandemic,” Peterson-KFF Health System Tracker, 4/24/23.

LGBTQ youth are in a mental health crisis: 41% of LGBTQ young people seriously considered attempting suicide within the last year, and 14% actually attempted it, with even higher rates being reported among transgender youths, nonbinary youths, and youths of color. 56% of LGBTQ young people who wanted mental health care were not able to get it. Just 38% of LGBTQ young people found their home to be LGBTQ-affirming. Nearly 1 in 3 LGBTQ young people said their mental health was poor most of the time or always due to anti-LGBTQ policies and legislation. Nearly 2 in 3 LGBTQ young people said that hearing about potential state or local laws banning people from discussing LGBTQ people at school made their mental health a lot worse. The Trevor Project, “2023 U.S. National Survey on the Mental Health of LGBTQ Young People,” 5/1/23.

Many Black Americans live in cardiological care deserts: An estimated 16.8 million Black Americans live in counties with limited access to cardiology specialists, with over 2 million of these living in counties with no cardiologists whatsoever. Residents in these counties may have to commute well over 80 miles to receive cardiological care. Heart disease is the leading cause of death for non-Hispanic Black men and women, and predominantly Black counties have an average score of 4.6 on the cardiovascular risk index, as compared to the national average of 2.9. Cisneros, “More Than 16 Million Black Americans Live in Counties With Limited or No Access to Cardiologists,” GoodRx, 5/2/23.

Inequities exist in treatment of opioid use disorder: Although Black people in the United States have seen a greater increase in opioid overdose-related mortality than other groups since 2010, racial differences in prescription of medications used to treat addiction remain. A sample of Medicare claims data from 2016-2019 identified 25,9054 events related to opioid use disorder. Of these, 15.2% were in Black patients, 8.1% in Hispanic patients, and 76.7% in White patients. Buprenorphine was given after 12.7% of events in Black patients, compared with 18.7% in Hispanic patients and 23.3% in White patients. Naloxone was given after 14.4% of events in Black patients, compared with 20.7% in Hispanic patients and 22.9% in White patients. Benzodiazepines were given after 23.4% of events in Black patients, compared with 29.6% in Hispanic patients and 37.1% in White patients. Barnett et al., “Racial Inequality in Receipt of Medications for Opioid Use Disorder,” New England Journal of Medicine, 5/11/23.

Even highly rated hospitals give disparate care: Across all hospitals in a study of more than 10 million patients in 15 states, Black and Latino patients experienced 34% higher rates of sepsis after surgery than white patients, and Black patients experienced 51% higher rates of dangerous blood clots as surgery-related complications. Even at “A”-rated hospitals, the rate of perioperative hemorrhage in white patients was 2.01 cases per 1,000 at-risk discharges, compared with 2.80 cases for Black patients. Devereaux, “Health, safety disparities persist in highly rated hospitals: Leapfrog Group,” Modern Healthcare, 6/7/23.

Coverage Matters

Insurance coverage moderates inequalities in cancer diagnosis: Among women with cervical cancer, non-White women of all studied racial and ethnic groups had lower proportions of diagnosis of early-stage cancer. In terms of coverage, 57.8% of women with private or Medicare insurance received an early-stage diagnosis, compared with 41.1% of women with Medicaid or who were uninsured. More than half of the racial and ethnic inequities in diagnosis of advanced-stage cancer were found to be associated with lack of insurance coverage, ranging from 51.3% for Black women to 55.1% for Hispanic or Latina women. Holt et al., “Mediation of Racial and Ethnic Inequities in the Diagnosis of Advanced-Stage Cervical Cancer by Insurance Status,” JAMA Network Open, 3/10/23.

Veterans struggle with financial burdens of health care: 12.8% of veterans reported problems paying medical bills, 8.4% had foregone medical care, and 38.4% were somewhat or very worried about paying medical bills if they got sick or had an accident. The percentage of veterans somewhat worried about paying medical bills was lower for veterans with VA health care only (22.8%) and those with Tricare (16.3%) compared to veterans with private insurance, both with VA health care (33%) and without VA health care (30.2%). Cohen and Boersma, “Financial Burden of Medical Care Among Veterans Aged 25–64, by Health Insurance Coverage: United States, 2019–2021,” National Center for Health Statistics, 3/22/23.

Uninsured face disparities in cancer risk factors: While 12% of Americans smoked cigarettes in 2021, 20% of the uninsured smoked. Quit ratios among those who have smoked were lower for the uninsured as well, with 67% overall vs. 40% for the uninsured. 64% of women aged 45 years and older were up to date with breast cancer screening, but only 29% of uninsured women. 75% of women 25-65 were up to date with cervical cancer screening, but only 58% of uninsured women. 59% of adults 45 years and older were up to date with colorectal cancer screening, but only 21% of uninsured adults. American Cancer Society, “Cancer Prevention & Early Detection: Facts & Figures 2023-2024,” 5/2/23.

Anti-poverty programs ameliorate brain development and mental health issues: Programs like TANF and Medicaid reduce neurological issues associated with child poverty. For example, in some states, disparities in hippocampal volume between high and low income children were 43% smaller in states that expanded Medicaid than those that did not. Disparities in internalization of psychological issues between high and low income children were similarly smaller in Medicaid-expanding states than non-Medicaid-expanding states. Weissman et al., “State-level macro-economic factors moderate the association of low income with brain structure and mental health in U.S. children,” Nature Communications, 5/2/23.

Vulnerable mothers depend on Medicaid or must self-pay: In 2021, 51.6% of births were covered by private insurance, 41% by Medicaid, 3.4% by other insurance, and 3.9% by self-pay. Self-paying mothers were more likely to receive late or no prenatal care. 78.8% of mothers under 20 were on Medicaid, compared with 27.4% of mothers aged 35 and over. Just 10.4% of mothers with less than a high school education had private insurance, compared with 84.8% of mothers with a bachelor’s degree or higher. Similarly, mothers with less than a high school education were most likely to self-pay at 13.2%. Among Black and Hispanic mothers, 64% and 58.1% of deliveries, respectively, were covered by Medicaid, compared with 22.5% of Asian, 23.2% of American Indian or Alaska Native, 28.9% of Native Hawaiian or other Pacific Islander, and 28.1% of white mothers. Valenzuela, “Characteristics of Mothers by Source of Payment for the Delivery: United States, 2021,” National Center for Health Statistics, May 2023.

Profiteers in Health Care

Hospital industry group narrative does not match data: Despite claims from these groups that hospitals are in a dire financial situation, profit margins hit all-time highs in 2021, and hospitals received almost $200 billion in government subsidies. In addition, tax exemptions for nonprofit hospitals in 2020 were estimated at around $28 billion, nearly double the total cost of charity care provided by these hospitals at $16 billion. Herman, “Hospitals are not crumbling, Medicare experts tell Congress,” STAT News, 3/20/23.

Cigna denies claims without reading them: Over a period of two months in 2022, Cigna denied over 300,000 requests for payment, spending an average of 1.2 seconds on each case. A single medical director working for the insurer reportedly rejected roughly 60,000 claims in one month. Corporate documents show that Cigna estimated only 5% of people would appeal a denial from their system. Rucker et al., “How Cigna Saves Millions by Having Its Doctors Reject Claims Without Reading Them,” ProPublica, 3/25/23.

Nonprofit hospitals do not spend enough on charity care: Of 1773 nonprofit hospitals evaluated, 77% spent less on charity care than they received in tax breaks (referred to as a “fair share deficit”). The total of all fair share deficits amounted to $14.2 billion–enough to erase the medical debts of 18 million Americans or rescue 600 rural hospitals from closure. Many of the hospitals with the largest deficits received millions in COVID-19 relief aid and ended the year with high net incomes. The hospital with the highest fair share deficit, UPMC Presbyterian Shadyside, saw a difference of $246 million. Lown Institute, “Fair Share Spending, 2023,” 4/11/23.

Health insurance CEOs see record-breaking salaries: In 2022, the CEOs of the seven major publicly traded health insurance and services conglomerates — CVS Health, UnitedHealth Group, Cigna, Elevance Health, Centene, Humana, and Molina Healthcare — combined to make more than $335 million. This number is 18% higher than the previous record from 2021, mostly due to increasing stock prices. Just one executive, Joseph Zubretsky of Molina, made $181 million as head of a company that owes 80% of its revenue to Medicaid programs. Herman, “Health insurance CEOs set another record for pay in 2022,” STAT News, 4/27/23.

Studies and analysis of interest to single-payer advocates

“Century-Long Trends in the Financing and Ownership of American Health Care,” by Adam Gaffney, M.D., M.P.H.; Steffie Woolhandler, M.D., M.P.H.; and David U. Himmelstein, M.D., The Milbank Quarterly, 4/24/23. “Over the past century, the tax-financed share of health care spending has risen from 9% in 1923 to 69% in 2020; a large part of this tax financing is now the subsidization of private health insurance. For-profit ownership of health care facilities has also increased in recent decades and now predominates for many health subsectors. A rising share of physicians are now employees. US health care is, increasingly, publicly financed yet investor owned, a trend that has been accompanied by rising medical costs and, in recent years, stagnating or even worsening population health.”

“The Association of Childbirth with Medical Debt in the USA, 2019-2020,” by Jordan Cahn M.D., M.Sc.; Ayesha Sundaram M.D.; Roopa Balachandar M.D.; Alexandra Berg M.D.; Aaron Birnbaum M.D.; Stephanie Hastings D.O.; Matthew Makansi M.D.; Emily Romano M.D.; Ariel Majidi M.D.; Danny McCormick M.D., M.P.H.; & Adam Gaffney M.D., M.P.H., Journal of General Internal Medicine, 5/18/23. “Postpartum women experience higher levels of medical debt than other women; poorer women and those with common chronic diseases may have an even higher burden. Policies to expand and improve health coverage for this population are needed to improve maternal health and the welfare of young families.”

“The $20 Billion Scam At The Heart Of Medicare Advantage,” by Matthew Cunningham-Cook and Andrew Perez, The Lever, 5/26/23. “Humana is the most prominent example of how insurers have built a major cash cow out of systematically overbilling Medicare Advantage, the private Medicare program operated by private interests. These overpayments are symptomatic of a broader profit-driven policy agenda that seeks to completely privatize Medicare, one of the nation’s most popular social programs, and lock program recipients into subpar private insurance plans, even when they get sicker and need the best care possible.”

“Projected Health Outcomes Associated With 3 US Supreme Court Decisions in 2022 on COVID-19 Workplace Protections, Handgun-Carry Restrictions, and Abortion Rights,” by Adam Gaffney, M.D., M.P.H.; David U. Himmelstein, M.D.; Samuel Dickman, M.D.; Caitlin Myers, Ph.D.; David Hemenway, Ph.D.; Danny McCormick, M.D., M.P.H.; Steffie Woolhandler, M.D., M.P.H., JAMA Network Open, 6/1/23. “Outcomes from 3 Supreme Court decisions in 2022 could lead to substantial harms to public health, including nearly 3000 excess deaths (and possibly many more) over a decade.”

“It’s Not Just You: Many Americans Face Insurance Obstacles Over Medical Care and Bills,” by Reed Abelson, New York Times, 6/15/23. “The survey also underscored the persistent problem of affordability as people struggled to pay their share of health care costs. About 40 percent of those surveyed said they had delayed or gone without care in the last year because of the expense. People in fair or poor health were more than twice as likely to report problems with paying medical bills than those in better health, and Black adults were more likely than white adults to indicate they had trouble.”

PNHP Chapter Reports

California

In California, multiple chapters have been at work on several initiatives. PNHP-Ventura members Dr. Helen Petroff and Dr. Leslie-Lynn Pawson attended the All Members Advocacy Meeting of the California Academy of Family Physicians (CAFP) in Sacramento. There, Dr. Petroff and Dr. Pawson presented testimony to the CAFP Board of Directors in support of their resolution supporting single payer. Members also conducted a presentation on single payer to the student volunteers and nursing staff at the WestMinster Free Clinic in Oxnard, CA, in order to build their pipeline of activists. PNHP-Humboldt has passed several resolutions against Medicare privatization, placed ads for universal health care in a local publication, and is currently promoting a presentation of the film “American Hospitals.” Multiple chapters also attended a protest against Rep. Kevin McCarthy to advocate for the protection of Social Security and Medicare.

To get involved in California, please contact Dr. Nancy C. Greep at ncgreep@gmail.com.

Maine

Members of Maine AllCare held a statewide town hall-style meeting with about 40 attendees, providing updates on chapter activities and hosting a Q&A. The chapter also completed a series of six lunchtime information sessions with state legislators on a variety of aspects of universal health care, including the effects of our current system on rural providers. Finally, outreach to the Maine congressional delegation on Medicare for All continues.

To get involved in Maine, please contact Karen Foster at kfoster222@gmail.com.

New York

In New York, PNHP-NY Metro had their annual Lobby Day in support of the NY Health Act. This year they took the special step of having the introductory cohort of their Universal Health Legislative Advocacy Fellowship schedule, coordinate, and lead the meetings. The chapter also hosted a forum on maternal health and the shortcomings of the current health system for mothers. Discussing how racism impacts quality of and access to care for mothers of color, the event highlighted the stories of a number of patients who spoke at a panel with birth workers. Finally, members held a showing of “American Hospitals” followed by a panel discussion.

To get involved in New York, please contact Mandy Strenz at mandy@pnhpnymetro.org.

North Carolina

In Charlotte, members of Healthcare Justice-NC spoke with HHS Secretary Xavier Becerra on his visit to North Carolina and encouraged him to reverse Medicare privatization via Medicare Advantage and ACO REACH. Members also participated in a health fair at Johnson C. Smith University, an HBCU in Charlotte. Board Member Dr. Doug Robinson gave the first of several mini-lectures to Mecklenburg County Commissioners to encourage them to pass a resolution supporting Medicare for All. Finally, chapter chair Dr. George Bohmfalk met with Georgia senator Jon Ossoff to discuss Medicare for All.

To get involved in Charlotte, please contact Dr. George Bohmfalk at gbohmfalk@gmail.com.

In Asheville, members of Health Care for All Western North Carolina (HCFAWNC) participated in the MLK Peace March and obtained signatures for the Medicare for All petition they’re presenting to the city council this year. Additionally, members held several presentations at local Democratic meetings and in retirement communities. Finally, the chapter presented a Medicare for All resolution to the Asheville Reparations Commission’s Health & Wellness Subcommittee, where it was well received.

To get involved in HCFA-WNC, please contact Terry Hash at theresamhash@gmail.com.

Oregon

In Oregon, members sponsored a panel at the Oregon Health Forum entitled “Lessons from Abroad: What can other nations teach Oregon about efficient healthcare?” Panelists included Dr. Donald Berwick of Massachusetts, Dr. Irene Papanicolas of Brown University, Reginald Williams of the Commonwealth Fund, and Jack Friedman of PacificSource Health Plans. The moderator was Tina Edlund, former healthcare advisor to past governor Kate Brown. The chapter also issued a letter supporting full legislative funding of SB 1089, a bill to establish a universal health care plan for Oregon.

To get involved in Oregon, please contact Dr. Samuel Metz at pnhp@samuelmetz.com.

Pennsylvania

In Western Pennsylvania, members met with newly elected Rep. Chris Deluzio in advance of the release of the new Medicare for All bill. They discussed the health ramifications of the train derailment in East Palenstine, OH, which is located on the border of PA, in his district, and revisited the case of Libby, Montana, where the federal government provided Medicare for all residents of the area after a disaster. They also met with newly elected Congressional Rep. Summer Lee to discuss the release of the Medicare for All bill, and successfully encouraged her to sign on. Members also had several meetings with Allegheny County Council representatives to explore the possibility of placing a non-binding referendum supporting a single-payer health care system on the ballot.

To get involved in PNHP-Western Pennsylvania, please contact Judy Albert at jalbertpgh@gmail.com.

West Virginia

Our chapter in West Virginia continues to grow, and its website went live for the first time in March. Members have been holding regular monthly meetings with speakers on topics such as health care economics, social security, and updates from other state chapters. Efforts continue on membership recruitment at renewal at both state and national levels, as well as national phone banking efforts.

To get involved in West Virginia, please contact Dr. Daniel Doyle at doyledan348@gmail.com.

SNaHP Chapter Reports

SNaHP Ohio

The collection of chapters comprising SNaHP Ohio have come together to form the first statewide SNaHP Coalition, which they will use to organize, pass resolutions, and advocate for single payer health care at the state level. One of their first efforts was to pass a resolution at the Ohio State Medical Association eliminating previous policy language explicitly opposing Medicare for All and public options, which they successfully did. The group is also fundraising for organizations leading the Ohio abortion ballot initiative through sales of merchandise promoting Medicare for All.

To get involved with SNaHP Ohio, please contact Justin May at mayjf@mail.uc.edu.

Creighton University (Arizona)

SNaHP students at Creighton University in Arizona collaborated with the Creighton Justice in Medicine club to host a Single Payer 101 and myth-busting event and discussion, which was attended by over 20 students. The chapter also created a Political Advocacy Committee to write and pass resolutions, and met with organizers, PNHP members, and other students to plan a resolution campaign. Finally, members hosted events on health care economics and an educational event on ACO-REACH.

To get involved with SNaHP at Creighton University, please contact Allison Benjamin at allisonbenjamin7@gmail.com.

Dell University (Texas)

Students at Dell University in Texas held a lecture series over the course of a semester for medical students and undergrads on issues in the U.S. health system, the promise of single payer, and community organizing to achieve it. Featured speakers included Ed Weisbart, M.D. (PNHP), Liana Petruzzi, Ph.D. (UT Austin Social Work), Kellen Gildersleeve, R.N. (National Nurses United, Austin), Rachel Madley, Ph.D. (US Rep. Pramila Jayapal), and Yosha Singh, M.P.H. (Dell Med SNaHP). The chapter also worked with Austin City Council member Vanessa Fuentes to lobby the city to introduce a resolution in support of Medicare For All, which was passed in early May. Lastly, the chapter’s co-presidents wrote an op-ed on the urgency of Medicare For All and why it can particularly benefit Texas in the context of Medicaid unwinding after the public health emergency. The op-ed was published in the Austin Chronicle and was used as the basis for planning an op-ed workshop for our members which is forthcoming.

To get involved with SNaHP at Dell University, please contact Rohit Prasad at rohit.prasad@utexas.edu.

How You Can Support the Medicare for All Act

- Visit https://pnhp.org/legislation, where you can read about the bills and use our simple webform to send a cuztomizable email message to your representative and both of your senators, based on whether or not they have co-sponsored.

- Schedule an in-person meeting with your representative and with each of your senators—or with a health policy staffer at their district office.

- Write an op-ed or letter to the editor supporting the Medicare for All Act.

PNHP in the News

News items quoting PNHP members

“No, COVID-19 isn’t ‘over’—but millions of Americans’ Medicaid coverage is about to be,” The Real News Network, 4/7/23, featuring Dr. Margaret Flowers

“A conversation with doctors who support universal healthcare,” KALW, 4/12/23, featuring Dr. Susan Rogers

- “Medicare Advantage Industry ‘Scare Tactics’ and Lobbying Intensify Over Efforts to Curb Fraud,” Common Dreams, 3/21/23

- “149 Black healthcare leaders to know | 2023,” Becker’s Hospital Review, 4/26/23, featuring Dr. Claudia Fegan

- “We Don’t Just Need Medicare for All — We Need a National Health System,” Jacobin, 5/2/23, featuring Dr. Steffie Woolhandler and Dr. David Himmelstein

- “The Healthcare Long March: Why Exposing Evils of Medical Debt Doesn’t Fix the Problem,” FAIR, 5/8/23, featuring Dr. Johnathon Ross

- “‘Health care is a human right’: Morales proposes bill to create ‘Medicare for all’ healthcare system,” ABC 6, 5/15/23, featuring Dr. J. Mark Ryan

- “1 in 5 U.S. Seniors Now Skip Meds Because of Cost,” HealthDay, 5/22/23, featuring Dr. Adam Gaffney

Op-eds by PNHP members

- “Feeding time at the trough of Medicare,” by Dr. Robert S. Kiefner, Concord Monitor, 4/4/23

- “Medicare for All is the Timely Solution for Texas Health Care,” by Yosha Singh and Rohit Prasad, The Austin Chronicle, 4/14/23

- “We Can and Must Enact Medicare for All,” by F. Douglas Stephenson, LA Progressive, 5/31/23

- “A better health care system would ensure insurance for all,” by Dr. Norma Morrison, TimesNews, 6/1/23

- “The free market can’t save American health care,” by Dr. Jay Brock, Richmond Times-Dispatch, 6/4/23

- “What all seniors need to know about Medicare,” by Dr. Christine Llewellyn, Virginian-Pilot, 6/10/23

- “Why Are Corporate Healthcare Fraudsters Being Handed ‘Get Out of Jail Free Cards?” by Kay Tillow, Common Dreams, 6/12/23

- “Medicaid ‘unwinding’ is pulling the rug from under us,” by Dr. Jane Katz Field, VT Digger, 7/23/23

Letters to the editor by PNHP members

- “Even with Obamacare, Americans aren’t getting adequate health care,” by Dr. Jay Brock, Washington Post, 3/12/23

- “Support ‘Medicare for All’ legislation,” by Dr. Mark Pettus, The Berkshire Eagle, 4/22/23

- “Medicaid Options for Arizonans: Medicare for All Best,” by Dr. Joanne Mallett, Arizona Daily Star, 5/2/23

- “People wouldn’t be kicked off Medicaid if we had Medicare-for-all,” by Richard Bruning, Washington Post, 5/18/23

- “The case for single-payer health care in Massachusetts,” by Dr. Henry Rose, The Berkshire Eagle, 5/27/23

- “When Corporations Take Over Health Care,” by Dr. Cheryl Kunis, New York Times, 5/21/23

- “Documentary focuses on health systems,” by Patty Harvey, Times Standard, 5/25/23

- “Physicians’ group fights health-care discrimination,” by Dr. Leonardo Alonso, Orlando Sentinel, 6/16/23

- “Medical care should be available to all,” by Richard Bruning, Baltimore Sun, 6/18/23

- “Single-payer system would eliminate need for nurse-staffing laws,” by Dr. Daniel Bryant, Portland Press Herald, 7/5/23

Previous Experience: At the Jane Addams Senior Caucus, I built a powerful base of leaders who were bonded not by candidates or party, but by a vision for a better future.

Previous Experience: At the Jane Addams Senior Caucus, I built a powerful base of leaders who were bonded not by candidates or party, but by a vision for a better future. Previous Experience: I previously worked in nuclear and cyber policy research at the Carnegie Endowment for International Peace in Washington, D.C.

Previous Experience: I previously worked in nuclear and cyber policy research at the Carnegie Endowment for International Peace in Washington, D.C.